Business Banking & Fintech Guide for International Entrepreneurs | 2026

Why Business Banking Is More Important Than Company Formation

Many entrepreneurs spend weeks comparing company formation providers.

Very few spend the same amount of time thinking about what happens after their company has been incorporated.

Yet in practice, your banking and payment infrastructure will influence your business every single day.

It determines how you receive customer payments.

How you pay suppliers.

How you manage different currencies.

How quickly you can expand into new markets.

How efficiently you control cash flow.

And how professionally your business operates on a global scale.

In other words, company formation creates your legal structure. Business banking creates your operational capability.

The two should never be viewed separately.

The Biggest Mistake International Entrepreneurs Make

One of the most common assumptions is:

“Once I register my UK company, opening a business bank account will be straightforward.”

Unfortunately, international business does not work that way.

Every bank, Electronic Money Institution (EMI) and payment provider applies its own independent compliance procedures before deciding whether to onboard a business.

These reviews are designed to understand:

- Who owns the company.

- What the business does.

- Where customers are located.

- How payments will be received.

- Which countries the business operates in.

- Expected transaction volumes.

- Potential compliance risks.

This means that company incorporation and financial onboarding are two completely separate processes.

Understanding this distinction from the beginning allows entrepreneurs to prepare more effectively and avoid unrealistic expectations.

The Three Pillars of International Business Finance

Rather than searching for a single “best” provider, successful entrepreneurs build a financial ecosystem that matches their business model.

In most cases, this ecosystem consists of three complementary categories.

1. Traditional Business Banks

Traditional banks are licensed banking institutions that typically offer services such as:

- Business current accounts

- International transfers

- Corporate debit cards

- Foreign exchange services

- Lending and credit facilities

- Savings products

- Merchant services (where applicable)

They are often suitable for businesses seeking long-term banking relationships and broader financial services.

2. Electronic Money Institutions (EMIs)

EMIs have become an important part of international business.

Many provide:

- Multi-currency accounts

- International payment capabilities

- Faster online onboarding

- Expense management tools

- Team access controls

- Currency conversion

- API integrations

- Digital-first account management

Depending on the provider, these services may be particularly attractive to technology companies, consultants, agencies and internationally focused businesses.

3. Payment Providers

Receiving customer payments is a different requirement from holding business funds.

Payment providers help businesses accept payments through:

- Online checkout pages

- Payment links

- Card payments

- Digital wallets

- Subscription billing

- Marketplace integrations

- International payment processing

Examples include solutions designed for e-commerce businesses, software companies, freelancers and online service providers.

Choosing the right payment infrastructure is just as important as choosing the right bank.

There Is No “Best” Fintech

One of the most common questions entrepreneurs ask is:

“Which fintech is the best?”

The honest answer is:

There is no universal answer.

The most suitable provider depends on your business.

For example:

A software company serving clients worldwide may have very different operational needs from:

- an Amazon seller,

- an international consultant,

- an import-export business,

- a recruitment agency,

- or an AI startup.

Rather than looking for the “best” provider, focus on finding providers whose services align with your business model, target markets and operational requirements.

The Financial Ecosystem of a Modern International Business

The strongest international businesses rarely rely on a single financial provider.

Instead, they build an ecosystem where different services work together.

A typical setup may include:

- A business banking solution for day-to-day operations.

- A payment provider for customer transactions.

- Multi-currency capabilities for international trade.

- Professional accounting systems.

- Compliance processes.

- Cash flow management.

Each element plays a different role in supporting the business as it grows.

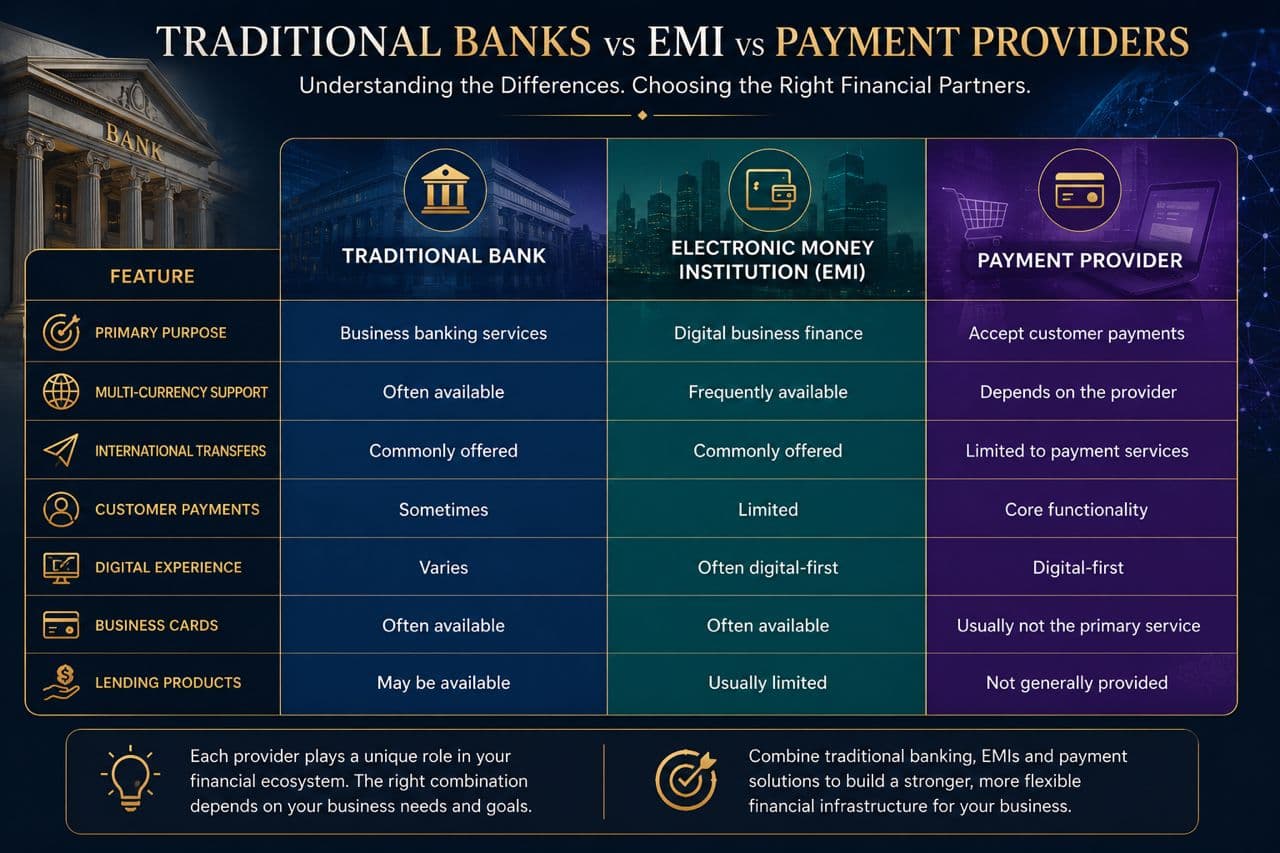

Traditional Banks, FinTechs & Payment Providers: Understanding the Difference

One of the biggest misconceptions among international entrepreneurs is believing that every financial institution provides the same services.

They do not.

In reality, the financial ecosystem is made up of different types of providers, each designed to solve different business needs.

Understanding these differences before applying can save considerable time and help you choose solutions that align with your business model.

Rather than asking:

“Which provider is the best?”

A better question is:

“Which combination of financial solutions best supports my business?”

Successful international businesses rarely rely on a single provider.

Instead, they build an ecosystem.

The Three Financial Pillars

Every internationally focused business generally relies on three categories of financial providers.

1. Traditional Business Banks

Traditional banks are licensed banking institutions that provide a broad range of financial services.

Depending on the institution, services may include:

- Business current accounts

- Domestic and international transfers

- Foreign exchange services

- Business debit and credit cards

- Lending facilities

- Savings products

- Trade finance

- Merchant services

Many established businesses value long-term banking relationships, particularly where lending, financing or complex international transactions are important.

2. Electronic Money Institutions (EMIs)

Electronic Money Institutions have transformed international business banking.

They are particularly popular among digital businesses because many offer:

- Multi-currency accounts

- Faster online onboarding

- International transfers

- Expense management

- Team access controls

- Currency exchange

- API integrations

- Digital account management

For software companies, consultants, agencies and online businesses, EMIs often provide flexibility that complements traditional banking.

Each provider has its own onboarding requirements, supported jurisdictions and service offering.

3. Payment Providers

Receiving payments is not the same as holding business funds.

Payment providers specialize in helping businesses accept customer payments through:

- Online card payments

- Payment links

- Subscription billing

- Checkout pages

- Marketplace integrations

- Digital wallets

- Mobile payments

These services are particularly relevant for:

- E-commerce businesses

- SaaS companies

- Digital agencies

- Freelancers

- Consultants

- Online education businesses

Where Does PayPal Fit?

One of the most frequently asked questions from international entrepreneurs is:

“Do I need PayPal?”

The answer depends entirely on your business model.

PayPal is primarily a payment platform, not a replacement for your overall banking infrastructure.

For many businesses, it can be useful for receiving payments from customers who prefer PayPal as a checkout option.

For example, it is commonly used by:

- Freelancers

- Digital agencies

- Consultants

- Shopify stores

- eBay sellers

- International service businesses

However, PayPal is only one part of a wider payment strategy.

Many businesses combine PayPal with other payment solutions depending on their customers, products and sales channels.

Like other financial providers, PayPal applies its own onboarding, verification and compliance requirements.

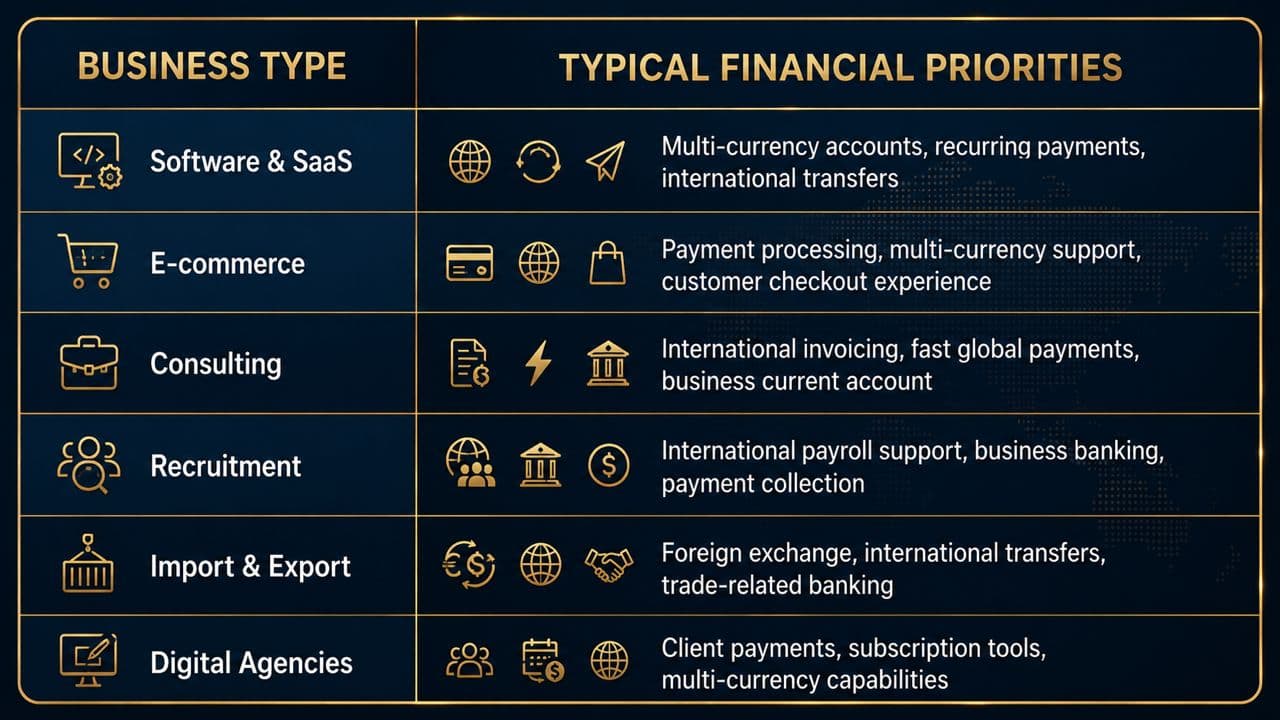

Choosing the Right Financial Ecosystem

Every business is different.

Below are examples of how different business models may prioritize different financial services.

here is no universal solution.

The most appropriate setup depends on your operational needs, customer locations and long-term strategy.

Why Onboarding Is Different for Every Provider

A common misconception is that if one provider declines an application, every other provider will reach the same decision.

That is not necessarily the case.

Every bank, EMI and payment provider has:

- Its own onboarding procedures.

- Independent compliance policies.

- Different risk appetites.

- Different supported industries.

- Different geographic availability.

- Different product features.

Understanding these differences helps entrepreneurs choose providers that are appropriate for their business rather than relying on assumptions.

Can One Provider Do Everything?

Sometimes.

But not always.

Many successful international businesses choose to diversify.

For example, they may use:

- One provider for everyday business banking.

- Another for international payments.

- A separate payment gateway for customer transactions.

- Additional accounting or expense management tools.

This approach can provide operational flexibility while allowing each solution to perform the role it is designed for.

The right structure depends on the specific needs of the business.

How Seven Oak Prestige Supports Clients

At Seven Oak Prestige, our objective extends beyond company formation.

We help international entrepreneurs understand the wider financial ecosystem that supports long-term business growth.

Where appropriate, we can introduce eligible clients to selected banking and fintech partners within our professional network.

These introductions are designed to help entrepreneurs explore suitable financial solutions based on their business activities and operational needs.

Every provider conducts its own independent onboarding, Know Your Customer (KYC), Anti-Money Laundering (AML) and risk assessment procedures.

For that reason, introductions should not be interpreted as a guarantee of account approval.

Our focus is on helping clients prepare professionally before they begin the onboarding process.

How Banks, Fintechs & Payment Providers Assess Your Business

Many entrepreneurs spend weeks comparing banking providers.

Far fewer spend time understanding how those providers evaluate their applications.

In reality, your preparation often has a greater influence on your onboarding experience than the provider you choose.

Whether you apply to a traditional bank, an Electronic Money Institution (EMI) or a payment provider, each organisation has one common objective:

To understand the business they are onboarding.

While every institution has its own policies and procedures, most compliance reviews are built around the same fundamental questions.

Understanding these questions before you apply allows you to prepare more effectively and present your business professionally.

Why Financial Institutions Carry Out Reviews

Banks, EMIs and payment providers operate within strict legal and regulatory frameworks.

As part of their responsibilities, they are generally required to understand:

- Who owns the business.

- What products or services the company provides.

- Where customers are located.

- How funds are expected to move.

- Whether the business activities align with their internal policies.

These reviews help institutions meet their legal obligations and manage financial crime risks.

For entrepreneurs, they are simply part of the onboarding process.

The Five Areas Most Providers Review

Although every provider has its own assessment process, applications are commonly reviewed across five key areas.

1. Your Business Model

One of the first questions reviewers ask is simple:

What does this business actually do?

Surprisingly, many entrepreneurs answer this too vaguely.

For example:

“Consulting”

“Trading”

“Technology”

These descriptions provide very little context.

A clearer explanation might be:

“We provide software development services for healthcare businesses in Europe and North America.”

Or:

“We operate a Shopify-based e-commerce business selling branded consumer products to customers in the UK, Europe and the United States.”

The clearer your business model, the easier it is for reviewers to understand your activities.

2. Your Online Presence

In today’s digital economy, your website is often one of the first places a compliance team looks.

A professional website helps explain:

- Your products or services.

- Your target customers.

- Your contact information.

- Your business location.

- Your company’s purpose.

A website that appears incomplete, inconsistent or outdated may generate additional questions during onboarding.

Think of your website as your digital business card.

3. Business Documentation

Financial institutions often request documentation to better understand your business.

Depending on the provider and your business activities, this may include information about:

- Company incorporation.

- Directors and shareholders.

- Business activities.

- Expected turnover.

- Source of funds.

- Supporting contracts or invoices.

Submitting complete and well-organised information from the outset can make the review process more efficient.

4. Expected Transaction Activity

Providers generally seek to understand how your account is expected to be used.

Examples may include:

- Typical transaction values.

- Expected monthly volume.

- Main customer locations.

- Main supplier locations.

- Currencies used.

- Frequency of international payments.

Providing realistic expectations helps reviewers build an accurate picture of your business.

5. Consistency

Perhaps the most underestimated factor is consistency.

Your company information should align across:

- Incorporation documents.

- Website.

- Business descriptions.

- Invoices.

- Banking applications.

- Payment provider applications.

Small inconsistencies can lead to additional questions and extend the review process.

Consistency builds confidence.

KYC and AML Explained in Simple Terms

Many entrepreneurs hear the terms KYC and AML without fully understanding what they mean.

Know Your Customer (KYC)

KYC refers to the process of verifying the identity of customers and understanding who they are.

This may involve reviewing identity documents and information about the business.

Anti-Money Laundering (AML)

AML refers to measures designed to help financial institutions detect and prevent financial crime.

These procedures are a normal part of onboarding and apply across much of the financial sector.

For legitimate businesses, KYC and AML are simply standard compliance requirements.

Why Some Applications Take Longer Than Others

A longer review period does not necessarily indicate that an application has been rejected.

In many cases, additional time is required because reviewers need further clarification.

Examples include:

- Business activities that are not clearly explained.

- Missing documentation.

- Inconsistent information.

- High levels of international activity requiring additional review.

- Requests for further verification.

Responding promptly and providing accurate information can help move the process forward.

Preparing Before You Apply

Rather than waiting until you submit an application, take time to prepare your business.

A professional business is easier to understand.

Consider whether you have:

A professional website.

A business email using your own domain.

A clear explanation of your products or services.

Accurate company information.

Supporting documentation organised.

A realistic understanding of your expected payment flows.

Preparation demonstrates professionalism and helps reviewers understand your business more efficiently.

Seven Oak Prestige’s Approach

At Seven Oak Prestige, we encourage entrepreneurs to prepare before they apply.

Our role is not to promise approvals.

Instead, we help clients establish a professional business foundation that supports future onboarding.

Where appropriate, we can introduce eligible clients to selected banking and fintech partners within our network.

Every provider independently assesses applications according to its own onboarding, KYC, AML and risk policies.

Good preparation does not guarantee approval, but it helps ensure your business is presented clearly, consistently and professionally.

Key Takeaway

The strongest applications are not always submitted by the largest companies.

They are often submitted by businesses that are well prepared.

Professional documentation.

A clear business model.

Consistent information.

An organized online presence.

These factors help financial institutions understand your business more effectively and support a smoother onboarding experience.

Building a Banking Strategy for Long-Term International Growth

Choosing a banking solution is not a one-time decision.

As your business grows, your financial requirements are likely to evolve.

A freelancer serving a handful of international clients today may become the founder of a software company processing payments in multiple currencies tomorrow.

An e-commerce business selling locally may later expand into Europe, North America or the Middle East.

The financial infrastructure that supports your business should be capable of evolving alongside your ambitions.

Rather than asking, “Which provider should I choose today?”, a better question is:

“Will my financial ecosystem continue to support my business as it grows?”

Thinking long-term from the beginning often reduces future operational challenges and allows entrepreneurs to scale with greater confidence.

Business Banking Is a Business Decision

Many founders compare providers based solely on fees.

While pricing is important, it should not be the only factor influencing your decision.

A banking or fintech solution should support the way your business operates.

Before choosing a provider, consider questions such as:

- Will you receive payments in multiple currencies?

- Do you expect to invoice international clients?

- Will your team need access to business accounts?

- Do you require integrations with accounting software?

- Will your business expand into additional countries?

- Do you expect increasing transaction volumes over time?

Selecting a provider that aligns with your operational needs is often more valuable than focusing only on the lowest cost.

Traditional Banks, EMIs and Payment Providers Can Work Together

Many entrepreneurs assume they must choose one provider for everything.

In reality, successful international businesses often combine different financial services.

For example, a company may use:

- A traditional bank for long-term business banking.

- An Electronic Money Institution (EMI) for multi-currency operations.

- A payment provider to accept customer payments online.

- Accounting software to manage financial records.

- Expense management tools to monitor company spending.

Each service performs a different function within the business.

Building the right combination creates a stronger and more flexible financial ecosystem.

Comparison: Traditional Banks vs EMIs vs Payment Providers

The appropriate combination depends on your business model, target markets and operational requirements.

Your International Banking Readiness Checklist

Before approaching any bank, EMI or payment provider, ask yourself:

Business Structure

UK company incorporated

Company information up to date

Registered Office Address arranged

Director information consistent

Professional Presence

Business website published

Business email using your own domain

Clear explanation of products or services

Privacy Policy and Terms available where appropriate

Documentation

Incorporation documents organised

Identification documents available

Proof of address prepared where required

Supporting business information ready

Financial Planning

Expected transaction profile understood

Main customer locations identified

Main supplier locations identified

Expected currencies considered

Estimated monthly turnover prepared

Compliance

Companies House obligations understood

HMRC responsibilities reviewed

VAT requirements considered where applicable

EORI requirements reviewed where relevant

Preparation helps create a more organised onboarding experience and demonstrates professionalism.

How Seven Oak Prestige Supports International Entrepreneurs

At Seven Oak Prestige, we believe that successful company formation extends beyond incorporation.

Our objective is to help international entrepreneurs establish a strong operational foundation from the beginning.

Depending on your business requirements, our support may include:

- UK Company Formation.

- Registered Office Address.

- Director Service Address.

- Companies House compliance guidance.

- Business banking preparation.

- Introductions to selected banking and fintech partners where appropriate.

- Guidance on payment solutions for international businesses.

- VAT and EORI assistance where applicable.

Every financial institution and payment provider conducts its own independent onboarding, KYC, AML and risk assessment procedures.

For this reason, no provider or intermediary can guarantee account approval.

Our role is to help entrepreneurs prepare professionally, understand the process and approach onboarding with confidence.

Frequently Asked Questions

Can a non-resident apply for business banking?

Many financial institutions and EMIs accept applications from international entrepreneurs, subject to their own eligibility criteria, onboarding procedures and compliance requirements.

Is one provider suitable for every business?

No.

The most appropriate financial solution depends on your business model, target markets, operational needs and long-term objectives.

Should I use both a bank and an EMI?

Many international businesses choose to combine different financial services to support different operational requirements.

The most suitable approach depends on your individual circumstances.

Does Seven Oak Prestige provide banking services?

No.

We are not a bank or an Electronic Money Institution.

We assist clients with UK company formation, business preparation and, where appropriate, introductions to selected banking and fintech partners.

All financial products remain subject to each provider’s independent assessment and approval process.

Final Thoughts

Building an international business requires more than choosing the right company structure.

It requires a financial ecosystem capable of supporting your operations today and adapting as your business grows.

The most successful entrepreneurs do not simply open an account.

They establish a strategy.

They prepare their documentation.

They present their business professionally.

They understand compliance.

And they select financial solutions that align with their long-term objectives.

By approaching business banking as part of a broader growth strategy, you create a stronger foundation for international success.

Whether you are launching your first UK company or expanding an established business into new markets, thoughtful preparation today can support sustainable growth for years to come.

Related Articles

Continue exploring our knowledge hub: